Luxury Industry Outlook 2026: Market Size, Trends & Global Influence

The global luxury market in 2026 emerges as a major economic force and cultural phenomenon, driven by wealth growth, digitalization, and evolving consumer values.

The Global Luxury Market 2026: Economic Powerhouse & Cultural Phenomenon

How Premier Brands Shape Global Commerce, National Economies, and Consumer Culture

World Biz Magazine: Luxury Industry & Market Analysis

Global Industry Overview

Luxury as a Strategic Economic Force

The global luxury and premier brands market has evolved far beyond its traditional perception as a niche sector serving elite consumers. Today, it represents a sophisticated economic ecosystem generating nearly $2 trillion in annual value, influencing manufacturing centers, tourism flows, employment patterns, cross-border trade, and national brand prestige across continents.

From the haute couture ateliers of Paris to the precision watchmaking workshops of Switzerland, from the automotive masterpieces of Italy and Germany to the rapidly expanding luxury retail landscapes of Shanghai, Dubai, and Mumbai, the luxury industry stands as both a guardian of traditional craftsmanship and a pioneer of digital innovation.

This is not merely an industry of expensive products it is a global cultural and economic phenomenon that shapes how nations position themselves in international markets, how cities attract tourism and investment, and how consumers worldwide express identity, achievement, and aspiration.

Defining the Modern Luxury Ecosystem

Contemporary luxury encompasses a sophisticated array of high-value categories unified by several defining characteristics:

Core Attributes:

· Superior craftsmanship, materials, and design excellence

· Strong brand heritage, storytelling, and cultural authenticity

· Exclusivity through limited production and premium pricing

· Emotional resonance and status-driven consumer value

· Innovation balanced with tradition and timeless appeal

Major Market Categories:

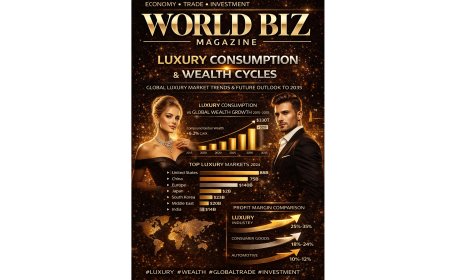

Personal Luxury Goods comprise fashion and accessories, leather goods and handbags, footwear, watches and jewelry, and beauty products and fragrances. This segment alone accounts for approximately $370-400 billion in annual sales.

Luxury Automobiles include premium and ultra-luxury vehicles characterized by bespoke customization options and cutting-edge engineering, representing a significant portion of luxury spending particularly in North America, Europe, and the Middle East.

Experiential Luxury has emerged as a defining trend, encompassing high-end hospitality and travel, private aviation and yachts, exclusive events and VIP access, and personalized services and concierge offerings. Modern consumers increasingly prioritize experiences over mere ownership.

Lifestyle & Collectibles round out the ecosystem with luxury home furnishings and design, fine art and auction markets, rare wines and spirits, and digital assets including NFTs and virtual luxury goods.

Market Size, Valuation & Growth Trajectory

The luxury market demonstrates remarkable resilience and sustained expansion across economic cycles.

Current Market Landscape (2025-2026):

· Total Global Luxury Market: $1.6-1.8 trillion (including travel, automobiles, and services)

· Personal Luxury Goods Segment: $296.9-400 billion

· Asia-Pacific Market Share: Nearly 40% of global luxury consumption

· Digital Penetration: Over 70% of luxury consumers engage with brands online; e-commerce represents 20%+ of total sales

Growth Forecast & Projections:

· 2030 Market Valuation: $2.4-2.6 trillion

· 2034 Personal Luxury Goods: $407.2 billion

· Compound Annual Growth Rate (CAGR 2026-2034): 3.6-8% depending on category and region

· Long-term Scenario (2035): Potential expansion beyond $500 billion in personal luxury goods under favorable digital adoption and global wealth growth scenarios

These projections reflect sustained premiumization trends, expanding global wealth, rising aspirational consumption in emerging markets, and successful digital transformation across the industry.

Key Growth Drivers Reshaping the Industry

1. Global Wealth Expansion & Demographic Shifts

The proliferation of high-net-worth individuals (HNWIs) and ultra-high-net-worth individuals (UHNWIs) continues accelerating, particularly across Asia-Pacific, the Middle East, and select Latin American markets. Emerging affluent middle classes in countries like India, Indonesia, Vietnam, and Brazil represent untapped growth frontiers with expanding purchasing power and increasing brand awareness.

2. Generational Consumer Revolution

Millennials and Generation Z now account for over 60% of luxury purchases, fundamentally reshaping industry priorities. These demographics value sustainability and ethical production, demand authentic brand storytelling and cultural relevance, expect seamless digital experiences and personalization, and prioritize experiential luxury alongside product ownership. Their influence has accelerated industry transformation toward transparency, innovation, and social responsibility.

3. Digital Transformation & Technology Integration

The luxury sector has embraced comprehensive digital strategies including sophisticated e-commerce platforms with immersive experiences, virtual reality showrooms and augmented reality try-on capabilities, blockchain authentication and provenance tracking, AI-driven personalization and customer intelligence, and exploration of metaverse presence and virtual luxury assets. Online luxury sales continue growing at double-digit rates, forcing traditional brands to reimagine the relationship between physical and digital retail.

4. Tourism & Cross-Border Consumption

Luxury retail remains intimately connected to global travel patterns. Major cities like Paris, Milan, London, Dubai, Singapore, Hong Kong, New York, and Tokyo serve as luxury shopping destinations where tourism-driven sales often exceed domestic consumption. Duty-free shopping and destination retail experiences represent critical revenue streams, making the industry vulnerable to travel disruptions but highly rewarding during periods of robust international mobility.

5. Sustainability & Ethical Luxury Movement

Consumer demand for environmental responsibility, transparent supply chains, ethically sourced materials, circular economy models including resale and recommerce, and social impact has transitioned from niche concern to mainstream expectation. Leading luxury houses have committed to carbon neutrality targets, sustainable material innovation, and supply chain transparency recognizing that long-term brand equity depends on alignment with evolving consumer values.

Geographic Market Leadership: Regional Dynamics

Asia-Pacific: The Growth Engine

The Asia-Pacific region has emerged as the epicenter of luxury market expansion, commanding nearly 40% of global market share with continued growth trajectory.

China stands as the world's largest luxury consumer market, with domestic consumption rebounding strongly and Chinese consumers accounting for roughly one-third of global luxury purchases. The market has matured beyond logo-driven consumption toward appreciation of craftsmanship, heritage, and understated luxury. Government policies, economic conditions, and consumer confidence significantly impact global luxury performance.

Japan maintains exceptionally high per-capita luxury spending, characterized by sophisticated consumer tastes, strong appreciation for quality and detail, and loyalty to established luxury brands. The market favors watches, jewelry, and premium fashion with particular emphasis on craftsmanship excellence.

India represents the fastest-growing major luxury market, experiencing double-digit expansion driven by a rapidly expanding affluent class, increasing international brand presence, urbanization and retail infrastructure development, and growing cultural acceptance of luxury consumption. Major brands view India as a strategic priority for the next decade.

South Korea demonstrates luxury growth led by beauty and cosmetics, fashion and accessories, and strong digital engagement, particularly among younger consumers who blend Korean and international luxury brands seamlessly.

Southeast Asia including Singapore, Hong Kong (as regional retail hubs), Thailand, Vietnam, Indonesia, and Malaysia shows emerging luxury demand with increasing urbanization and rising middle-class prosperity creating new opportunities for market entry and expansion.

Europe: Heritage & Manufacturing Excellence

Europe combines unparalleled luxury manufacturing heritage with strong domestic consumption and tourism-driven retail.

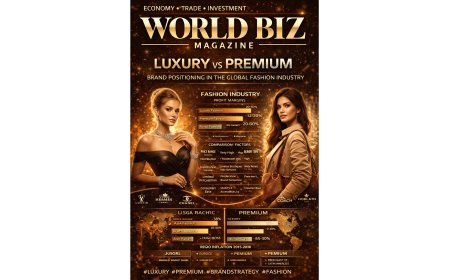

France serves as the global luxury capital, where the luxury sector contributes over 4% of national GDP. French luxury encompasses fashion houses (Louis Vuitton, Chanel, Hermès, Dior), beauty and fragrance leadership, wines and spirits, and significant employment across design, manufacturing, and retail. Luxury exports represent a cornerstone of French economic strategy and cultural diplomacy.

Italy excels in fashion and leather goods (Gucci, Prada, Bottega Veneta), luxury automotive excellence (Ferrari, Lamborghini, Maserati), artisanal manufacturing clusters, and contributes roughly 3% of national economic output through luxury activities, supporting thousands of small and medium enterprises and preserving traditional craftsmanship.

Switzerland dominates global luxury watchmaking, with watch exports valued in tens of billions annually, employing tens of thousands of skilled craftspeople in precision manufacturing, and maintaining Switzerland's reputation for quality, reliability, and technical excellence across luxury categories.

United Kingdom anchors European luxury with iconic British brands (Burberry, Mulberry), London as a global luxury retail destination, strength in bespoke tailoring and accessories, and significant luxury automotive presence.

Germany contributes through premium automotive leadership (Mercedes-Benz, BMW, Porsche, Audi), precision engineering and manufacturing, and growing strength in luxury lifestyle categories.

North America: Consumption Leadership

United States represents the largest single-country luxury market by revenue, characterized by high disposable income and strong consumer spending, diverse luxury consumption across all categories, robust demand for watches, jewelry, fashion, and automobiles, and sophisticated digital luxury adoption. American consumers value innovation, brand storytelling, and personalized experiences alongside traditional luxury attributes.

Canada maintains steady luxury consumption with concentration in major urban centers and strong tourism-linked luxury retail in cities like Vancouver and Toronto.

Middle East & Africa: Rapid Expansion

The Middle East has emerged as a critical luxury growth region driven by high-net-worth populations and tourism strategies.

United Arab Emirates, particularly Dubai and Abu Dhabi, functions as the luxury retail hub for the broader region, offering extensive luxury mall infrastructure, duty-free shopping advantages, and luxury positioning as part of national economic diversification. The UAE luxury market demonstrates consistently strong growth across all categories.

Saudi Arabia is experiencing rapid luxury market expansion under Vision 2030 economic transformation, with major retail developments, increasing luxury brand presence, growing domestic consumption, and openings to international tourism creating substantial opportunities.

Qatar shows high per-capita luxury spending supported by substantial wealth concentration and ongoing infrastructure and tourism development.

South Africa and Nigeria represent emerging luxury opportunities within the African continent, though market development remains nascent compared to other regions.

Latin America: Emerging Affluence

Brazil leads regional luxury consumption with growing affluent populations in São Paulo and Rio de Janeiro, and increasing international brand presence despite economic volatility.

Mexico benefits from proximity to the United States, expanding upper-middle class, and strong luxury retail in Mexico City and resort destinations.

Argentina, Colombia, and Chile show selective luxury growth concentrated in capital cities and among established wealthy populations.

Manufacturing Excellence: Where Luxury Is Created

Luxury production remains geographically concentrated, preserving centuries-old traditions while embracing modern innovation.

Traditional Manufacturing Powerhouses:

Italy excels in leather goods and accessories craftsmanship, fashion and textile production in regions like Tuscany and Veneto, footwear manufacturing with generational expertise, and artisanal production methods maintained through family businesses and specialized training programs.

France leads in haute couture and fashion manufacturing, perfume and cosmetics production centered in Grasse and Paris, luxury leather goods, and wine and spirits production requiring terroir-specific expertise and heritage techniques.

Switzerland maintains dominance in mechanical watchmaking through highly skilled watchmakers, precision engineering capabilities, vertical integration of component production, and protected designations of origin ensuring authenticity and quality.

Germany contributes advanced automotive engineering and manufacturing, precision instruments and technology, and increasingly sustainable luxury production methods.

Japan offers precision manufacturing and quality control, advanced materials science and innovation, high-end electronics and technology integration, and traditional craftsmanship in categories like Japanese denim and ceramics.

Emerging Production Centers:

Portugal has grown in footwear and leather goods production, textile manufacturing for luxury brands, and attracting international luxury production due to skilled labor and competitive costs.

Spain provides leather goods and accessories manufacturing, textile production, and traditional craftsmanship in select categories.

China (high-end segment) increasingly hosts advanced manufacturing for global luxury brands, sophisticated production capabilities with quality control, domestic luxury brand development, and serves as a critical distribution and customization hub for the Asia-Pacific region.

Turkey contributes luxury textile production, leather goods manufacturing, and serves as a bridge between European and Middle Eastern luxury markets.

India demonstrates growing luxury manufacturing capabilities, particularly in jewelry and gemstone processing, textile and embroidery work, and supporting artisanal production for both domestic and international brands.

Economic Impact: National & Fiscal Contributions

The luxury industry generates substantial economic value beyond direct sales, influencing employment, exports, tourism, tax revenues, and national branding.

Employment & Workforce Impact:

The global luxury sector directly employs over one million people in manufacturing, retail, design, and services, with additional millions in supporting industries including raw materials and component suppliers, logistics and distribution, marketing and creative services, and hospitality and tourism sectors. In Europe alone, luxury manufacturing sustains hundreds of thousands of skilled positions, often in regions where alternatives are limited.

Trade & Export Contributions:

Luxury goods represent high-value exports critical to trade balances. France's luxury exports exceed tens of billions of euros annually, supporting the national trade surplus. Italy's fashion and luxury automotive exports contribute similarly substantial amounts to trade performance. Switzerland's watch exports, valued in the tens of billions of francs, represent a cornerstone of Swiss export strategy. These export flows support currency strength, economic stability, and international competitiveness.

Fiscal Revenues & Tax Contributions:

Luxury consumption generates significant public revenues through value-added taxes and consumption levies, import duties and tariffs, corporate taxes from luxury companies, and employment-related taxes and social contributions. In markets like Japan, China, the European Union, and the United States, luxury-related tax revenues contribute billions annually to public finances, supporting social services, infrastructure, and public investment.

Tourism Multiplier Effects:

Luxury retail attracts international visitors, generating broader economic activity through hotel and hospitality spending, restaurant and entertainment consumption, transportation and related services, and destination marketing value. Cities like Paris, Milan, Dubai, and Singapore strategically position luxury retail as part of tourism development strategies, recognizing the substantial multiplier effects luxury shopping generates across the broader economy.

National Branding & Soft Power:

Luxury brands serve as cultural ambassadors, enhancing national prestige and international perception. French luxury reinforces France's cultural leadership, Italian luxury embodies Italian design excellence and dolce vita lifestyle, Swiss luxury guarantees precision and reliability, and British luxury conveys heritage and tradition. This soft power translates into tangible economic benefits through tourism, foreign investment, and international influence.

Industry Landscape: Global Players & Market Structure

The luxury ecosystem features a sophisticated mix of global conglomerates, independent heritage brands, and emerging players across categories.

Major Luxury Conglomerates:

LVMH (France) stands as the world's largest luxury conglomerate, encompassing over 75 brands across fashion and leather goods, wines and spirits, perfumes and cosmetics, watches and jewelry, and selective retailing. LVMH's brands include Louis Vuitton, Christian Dior, Fendi, Bulgari, TAG Heuer, Moët & Chandon, and Sephora.

Kering (France) controls a portfolio of distinctive luxury brands including Gucci, Saint Laurent, Bottega Veneta, Balenciaga, and Alexander McQueen, focusing on sustainable luxury and digital innovation.

Richemont (Switzerland) specializes in jewelry and watches through brands like Cartier, Van Cleef & Arpels, Jaeger-LeCoultre, IWC, and Piaget, commanding substantial market share in high jewelry and luxury timepieces.

Hermès (France) maintains independence with unparalleled craftsmanship heritage, iconic products including Birkin and Kelly bags, vertical integration of production, and exceptional brand equity built over generations.

Chanel (France) remains privately held with luxury fashion and accessories leadership, fragrance and beauty dominance, and commitment to French manufacturing and artisanal excellence.

Independent & Heritage Brands:

Rolex (Switzerland) dominates luxury watches with arguably the strongest brand recognition globally and unmatched retail demand.

Prada (Italy), Burberry (United Kingdom), and Salvatore Ferragamo (Italy) maintain independent luxury fashion positions.

Tiffany & Co. (now part of LVMH) represents American luxury jewelry heritage.

Swatch Group (Switzerland) encompasses multiple watch brands across price segments from accessible luxury to high complications.

Luxury Automotive Leaders:

Ferrari, Lamborghini, and Maserati (Italy) epitomize luxury automotive excellence. Porsche, Mercedes-Benz, BMW, and Audi (Germany) lead premium automotive segments. Rolls-Royce, Bentley, and Aston Martin (United Kingdom) represent ultra-luxury British automotive heritage.

Emerging & Digital-Native Luxury:

New players increasingly leverage digital platforms, sustainability positioning, and direct-to-consumer models, challenging traditional luxury distribution and brand-building approaches while established houses acquire or partner with innovative startups to access new capabilities and consumer segments.

Technology & Innovation: New Frontiers in Luxury

The luxury sector increasingly embraces technology while preserving core values of craftsmanship and heritage.

Digital Commerce & Customer Experience:

Advanced e-commerce platforms now offer immersive storytelling, high-resolution product visualization, seamless omnichannel experiences integrating online and offline touchpoints, and personalized recommendations driven by artificial intelligence and customer data platforms. Virtual and augmented reality enable virtual try-ons for watches, jewelry, and fashion, digital showrooms and brand experiences, and remote personal shopping consultations, extending luxury service models into digital environments.

Blockchain & Authentication:

Blockchain technology addresses counterfeiting and authentication challenges through digital certificates of authenticity, transparent provenance tracking from raw materials to finished products, and facilitation of authenticated luxury resale markets. NFTs and digital twins create new luxury asset classes and collector opportunities while providing additional authentication layers for physical products.

Sustainable Innovation:

Technology enables circular luxury models through resale and recommerce platforms like Vestiaire Collective and The RealReal, rental and subscription services democratizing access, and product lifecycle tracking and take-back programs. Materials innovation includes lab-grown diamonds and gemstones, sustainable leather alternatives and innovative textiles, recycled precious metals and responsible sourcing, and biodegradable packaging and reduced environmental footprint across the value chain.

Smart Manufacturing:

Luxury production increasingly incorporates advanced robotics for precision tasks while preserving handcraftsmanship, 3D printing for customization and prototyping, AI-driven quality control and production optimization, and digital supply chain management improving efficiency and transparency without sacrificing the human artistry that defines luxury.

Metaverse & Virtual Luxury:

Forward-looking brands experiment with virtual fashion and digital-only luxury items, branded experiences in gaming and virtual worlds, virtual stores and immersive brand environments, and digital collectibles and community building, recognizing that younger consumers increasingly value digital expression and virtual identity alongside physical ownership.

Emerging Trends & Future Market Dynamics

The Rise of "Quiet Luxury":

Consumer preferences are shifting toward understated elegance and craftsmanship over logo-driven consumption, quality and longevity over fast fashion principles, and timeless design over trend-driven purchasing. This reflects luxury market maturation and evolving definitions of status and success, particularly among younger wealthy consumers.

Personalization & Bespoke Services:

Luxury brands increasingly differentiate through made-to-order and customization options, exclusive limited editions and collaborations, personal shopping and concierge services, and intimate brand experiences and private events. Personalization extends beyond products to encompass entire customer journeys, creating deeper emotional connections and justifying premium pricing.

Wellness & Lifestyle Luxury:

The luxury sector expands into wellness-oriented categories including luxury fitness and wellness retreats, premium health and longevity services, high-end nutrition and supplements, and holistic lifestyle offerings. This reflects broader consumer priorities around health, wellbeing, and life quality over pure material accumulation.

Inclusivity & Accessibility Tensions:

Luxury brands navigate complex dynamics between maintaining exclusivity and brand prestige while expanding market access to younger and more diverse consumers, managing entry-level products without diluting brand equity, and balancing heritage with contemporary relevance and cultural sensitivity. Successful navigation of these tensions will separate market leaders from those left behind.

Geopolitical & Economic Headwinds:

The industry must adapt to economic volatility and consumer confidence fluctuations, currency exchange rate impacts on cross-border consumption, regulatory changes affecting trade and taxation, and geopolitical tensions influencing supply chains and market access. Recent luxury watch market volatility and shifting consumption patterns illustrate the sector's sensitivity to macroeconomic conditions despite general resilience.

Resale & Recommerce Growth:

The authenticated luxury resale market is expanding rapidly, driven by sustainability values among younger consumers, circular economy principles gaining acceptance, investment appeal of certain luxury categories, and digital platforms making resale accessible and trustworthy. Leading luxury houses now actively participate in resale markets, recognizing this as complement rather than competition to primary sales.

Long-Term Outlook: Luxury in 2030 and Beyond

As the luxury market approaches the next decade, several structural shifts will define its trajectory.

Continued Geographic Rebalancing:

Asia-Pacific will likely exceed 45-50% of global luxury consumption by 2030, with China maintaining market leadership while India and Southeast Asia accelerate growth. The Middle East will command increasing strategic importance through both domestic consumption and tourist-driven retail. Emerging markets in Latin America and Africa will contribute modestly but meaningfully to global growth, requiring patient brand building and market development.

Digital-First Operating Models:

Physical retail will remain important for brand experience and high-touch service, but luxury companies will operate on fully integrated digital foundations with seamless omnichannel capabilities, AI-driven personalization throughout customer journeys, comprehensive data analytics informing product development and marketing, and virtual experiences complementing physical touchpoints. Digital will represent 25-30% of luxury sales by decade's end.

Sustainability as Competitive Requirement:

Environmental and social responsibility will transition from differentiator to baseline expectation, with consumers and regulators demanding transparent and verifiable sustainability commitments, circular business models and take-back programs becoming standard, significant investment in sustainable materials and production innovation, and credible progress toward carbon neutrality and biodiversity protection. Brands failing to demonstrate authentic commitment will face reputational and commercial consequences.

Experiential Luxury Dominance:

The balance between product and experience will continue shifting toward experiential offerings including luxury travel and hospitality, exclusive events and access, personalized services and concierge capabilities, and brand-created content and entertainment. Luxury companies will evolve into lifestyle platforms orchestrating comprehensive experiences rather than simply producing high-end goods.

Innovation & Heritage Balance:

Successful luxury brands will master the delicate balance of preserving craftsmanship heritage and brand authenticity while embracing technological innovation and contemporary relevance, honoring historical brand codes while appealing to younger generations, and maintaining exclusivity while expanding global reach. This duality rooted in tradition yet forward-looking will define luxury leadership in coming decades.

Conclusion: Luxury Beyond Products

The global luxury and premier brands market represents far more than an industry of expensive goods. It embodies cultural expression, economic strategy, manufacturing excellence, and human aspiration. From its contributions to national GDP and employment to its influence on tourism, trade balances, and fiscal revenues, luxury has secured its position as a strategically significant economic sector with global reach and local impact.

As consumer values evolve toward sustainability, authenticity, and experience, and as global wealth continues redistributing toward Asia and emerging markets, the luxury sector faces both unprecedented opportunities and complex challenges. The industry's ability to innovate while preserving its heritage, to expand access while maintaining exclusivity, and to embrace responsibility while delivering desire will determine its continued relevance and prosperity.

For governments seeking to support high-value industries, investors evaluating long-term growth opportunities, brands navigating competitive dynamics, and consumers expressing identity and values through purchasing decisions, the luxury market will remain central to global commerce and culture throughout the coming decades.

The future of luxury lies not in denying change, but in leading it—transforming while remaining timeless, expanding while staying exclusive, and serving new generations while honoring centuries of craftsmanship. In this paradox lies the enduring power and promise of the global luxury ecosystem.

Disclaimer

This article is published by World Biz Magazine for informational and analytical purposes. While every effort has been made to ensure accuracy based on publicly available market research, industry reports, and credible sources current as of publication, the luxury market is dynamic and subject to rapid change due to economic conditions, consumer trends, geopolitical events, and other factors.

Market valuations, growth forecasts, and projections presented herein are derived from multiple industry sources and represent estimates that may vary between research firms and methodologies. Actual market performance may differ materially from forecasts due to unforeseen circumstances.

This article does not constitute investment, financial, or business advice. Readers should conduct independent research and consult qualified professionals before making business, investment, or strategic decisions related to the luxury industry. Company and brand references are included for illustrative and educational purposes and do not constitute endorsements or recommendations.

World Biz Magazine and its contributors assume no liability for decisions made based on information contained in this publication. All opinions expressed are those of the editorial team based on available information and industry analysis.

For the most current market data, company performance, and industry developments, readers are encouraged to consult primary sources, official company disclosures, and specialized luxury market research firms.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0