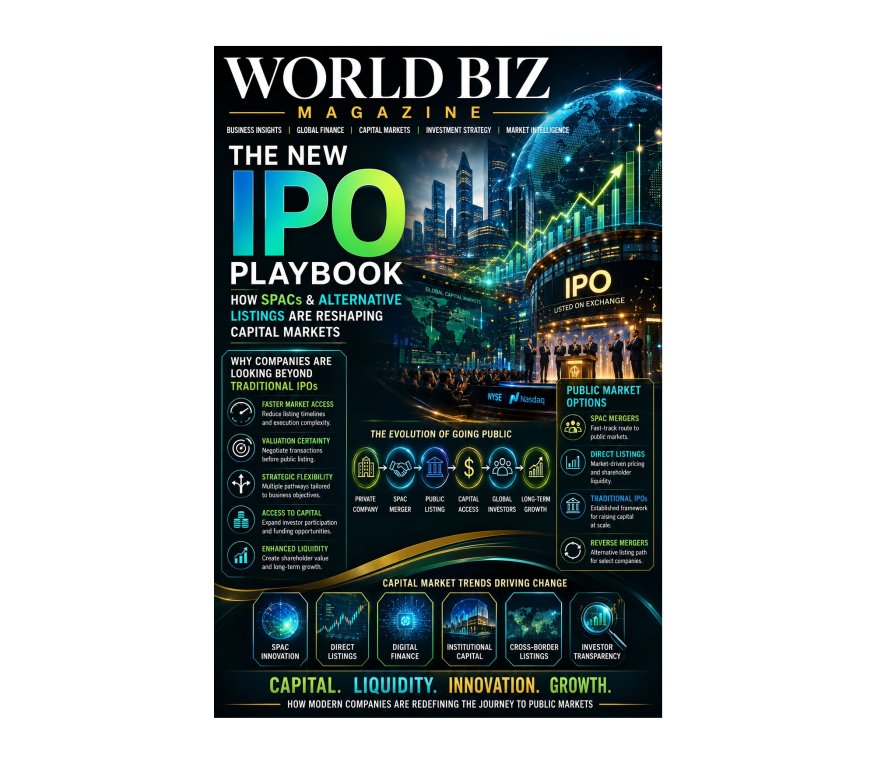

From IPOs to SPACs: Understanding Modern Routes to Public Company Status

A comprehensive guide to SPACs and alternative listing structures, including benefits, risks, regulations, investor considerations, and market trends.

Beyond the Traditional IPO: How SPACs and Alternative Listing Structures Are Reshaping Global Capital Markets

Examining the Rise of Special Purpose Acquisition Companies, Direct Listings, and Modern Pathways to Public Markets

World Biz Magazine | Capital Markets & Investment

For decades, the Initial Public Offering (IPO) served as the dominant gateway for private companies seeking access to public capital markets. From technology startups and manufacturing firms to healthcare innovators and consumer brands, the traditional IPO represented the gold standard for raising capital, expanding investor access, and enhancing corporate visibility.

However, the global capital markets landscape has undergone significant transformation in recent years. Increasing regulatory complexity, market volatility, rising underwriting costs, and evolving investor expectations have encouraged companies to explore alternative routes to public ownership. Among these alternatives, Special Purpose Acquisition Companies (SPACs) emerged as one of the most discussed financial innovations of the modern era, fundamentally changing how businesses approach public listings.

At the same time, direct listings, reverse mergers, dual-class structures, and other alternative listing mechanisms have gained attention as companies seek greater flexibility, faster execution, and improved control over valuation outcomes.

While traditional IPOs remain a critical component of global financial markets, today's corporate leaders, investors, and financial advisors are evaluating a broader range of listing structures than ever before. Understanding these alternatives has become increasingly important for businesses preparing for growth, liquidity events, strategic acquisitions, and long-term capital market participation.

This article explores the evolution of SPACs and alternative listing structures, examines their advantages and challenges, and analyzes their impact on the future of public market access.

The Evolution of Public Market Access

Historically, companies seeking public capital followed a relatively straightforward path.

The traditional IPO process typically involved:

- Selecting investment banks

- Conducting due diligence

- Preparing regulatory filings

- Marketing shares through roadshows

- Pricing the offering

- Listing on a public exchange

While effective, the IPO process often involves:

- Significant underwriting fees

- Lengthy preparation periods

- Regulatory complexity

- Market timing risks

- Valuation uncertainty

These challenges have encouraged innovation within capital markets.

As companies seek faster and more flexible listing options, alternative structures have gained prominence.

Understanding SPACs

A Special Purpose Acquisition Company (SPAC) is a publicly listed shell company created specifically to raise capital through an IPO with the intention of acquiring or merging with a private operating company.

SPACs are often referred to as: "Blank Check Companies."

· Unlike traditional operating businesses, SPACs have no commercial operations at the time of listing.

· Instead, they raise capital from investors and subsequently search for a private company to acquire.

· Once a suitable acquisition target is identified, the merger effectively takes the private company public.

This transaction is commonly known as a: De-SPAC Transaction

The process allows private companies to access public markets through merger rather than a conventional IPO.

How the SPAC Process Works

The SPAC lifecycle generally follows several stages.

Stage 1: SPAC Formation

Sponsors establish a shell company and prepare for an IPO.

These sponsors often include:

- Private equity executives

- Investment professionals

- Former CEOs

- Industry specialists

Stage 2: SPAC IPO

The SPAC raises capital from public investors.

Funds are typically placed in a trust account until an acquisition is completed.

Stage 3: Target Search

Sponsors identify a private company suitable for acquisition.

The search period commonly ranges from 18 to 24 months.

Stage 4: Acquisition Announcement

A proposed merger is announced to investors and regulators.

Detailed financial disclosures are provided.

Stage 5: Shareholder Approval

Investors vote on the proposed transaction.

Upon approval, the merger proceeds.

Stage 6: Public Market Listing

The private company becomes publicly traded through the completed merger.

The SPAC structure effectively disappears and is replaced by the operating company.

Why SPACs Became Popular

Several factors contributed to the rapid growth of SPAC activity.

Faster Access to Public Markets

Traditional IPOs may require extensive preparation periods.

SPAC mergers can often be completed more quickly.

Greater Valuation Certainty

In conventional IPOs, final valuations are often determined shortly before pricing.

SPAC transactions allow companies to negotiate valuation directly with sponsors.

Reduced Market Timing Risk

Companies can avoid some of the uncertainty associated with IPO roadshows and volatile market conditions.

Access to Experienced Sponsors

Many SPAC sponsors possess industry expertise, operational experience, and extensive investor networks.

This can create strategic advantages beyond capital raising.

Challenges and Criticisms of SPACs

Despite their benefits, SPACs have faced increasing scrutiny.

Regulatory Oversight

Regulators have introduced stricter disclosure requirements.

Investor protection has become a major focus.

Dilution Concerns

Sponsor incentives, warrants, and shareholder redemptions may dilute ownership.

This can impact long-term shareholder value.

Performance Variability

Many post-merger companies have experienced significant share price volatility.

Performance outcomes have varied considerably across transactions.

Investor Skepticism

As the SPAC market matured, investors became increasingly selective regarding target quality and valuation assumptions.

Direct Listings: Another Alternative to Traditional IPOs

Direct listings represent a different approach to public market access.

In a direct listing:

- Existing shareholders sell shares directly to public investors.

- No new shares are typically issued.

- Underwriting involvement is reduced.

- Market demand determines pricing.

This structure has been utilized by several high-profile technology companies seeking greater pricing transparency and lower issuance costs.

Advantages of Direct Listings

Reduced Dilution

Companies generally avoid issuing substantial new equity.

Lower Transaction Costs

Underwriting fees are often lower than traditional IPOs.

Market-Based Pricing

Pricing is determined through open market demand rather than investment bank allocations.

Increased Liquidity for Existing Shareholders

Early investors and employees may gain direct access to public market liquidity.

Challenges of Direct Listings

Limited Capital Raising

Traditional direct listings may not generate substantial new capital.

Greater Market Volatility

Without stabilization mechanisms, price fluctuations may be more pronounced.

Reduced Marketing Support

Companies often receive less promotional support compared to traditional IPOs.

Reverse Mergers

Another alternative listing structure involves reverse mergers.

In a reverse merger:

- A private company merges with an existing public company.

- The private company assumes control.

- Public listing status is retained.

This structure can accelerate public market access.

However, investors often conduct enhanced due diligence due to historical governance concerns associated with some reverse merger transactions.

Dual-Class Share Structures

Many modern public companies adopt dual-class share systems.

Under this approach:

- Founders retain enhanced voting rights.

- Public shareholders receive limited voting power.

- Management control remains concentrated.

Technology companies frequently utilize this structure to preserve strategic direction while accessing public capital.

Supporters argue it protects long-term innovation.

Critics argue it reduces shareholder accountability.

Traditional IPOs Remain Relevant

Despite the growth of alternative structures, traditional IPOs continue to play a central role in capital markets.

Advantages include:

- Broad investor participation

- Established regulatory frameworks

- Enhanced credibility

- Extensive analyst coverage

- Strong institutional demand

For many companies, the traditional IPO remains the preferred route to public ownership.

Comparing Public Listing Options

Traditional IPO

Best suited for:

- Established businesses

- Large capital raises

- Institutional investor participation

SPAC Merger

Best suited for:

- Companies seeking faster execution

- Businesses requiring valuation certainty

- Firms benefiting from sponsor expertise

Direct Listing

Best suited for:

- Well-capitalized companies

- Strong brand recognition

- Existing shareholder liquidity objectives

Reverse Merger

Best suited for:

- Smaller companies

- Accelerated listing timelines

- Specialized strategic situations

The Regulatory Environment

Regulators worldwide have increased scrutiny of alternative listing structures.

Areas of focus include:

- Investor protection

- Disclosure quality

- Governance standards

- Financial transparency

- Sponsor accountability

Future regulations will likely shape how these structures evolve.

Companies considering alternative listings must carefully evaluate compliance requirements.

The Future of Public Market Listings

Several trends are influencing the future of IPO markets.

These include:

- Digital capital raising platforms

- Greater institutional participation

- Cross-border listings

- Enhanced disclosure standards

- AI-driven investment analysis

- Private market growth

- Increased retail investor involvement

Public market access will likely continue evolving as technology, regulation, and investor behavior reshape financial ecosystems.

World Biz Magazine Insights

The rise of SPACs and alternative listing structures reflects a broader transformation within global capital markets. Companies today are demanding greater flexibility, faster execution, improved valuation transparency, and more strategic control over the public listing process. While traditional IPOs remain the benchmark for many organizations, alternative pathways have expanded the range of financing options available to growth-stage businesses. The future is unlikely to be dominated by a single listing structure; instead, successful companies will increasingly select pathways that best align with their capital requirements, governance objectives, investor base, and long-term strategic vision.

Conclusion

SPACs, direct listings, reverse mergers, and other alternative listing structures have fundamentally expanded the options available to companies seeking access to public capital markets. These alternatives offer unique advantages related to speed, flexibility, valuation certainty, and shareholder liquidity, while also presenting new regulatory, governance, and investor-relations challenges.

As capital markets continue evolving, companies must carefully assess which listing structure best supports their strategic objectives. Whether pursuing a traditional IPO, a SPAC merger, or another alternative pathway, the ultimate goal remains the same: accessing capital efficiently while creating long-term value for shareholders.

The continued evolution of listing structures demonstrates that public market access is no longer a one-size-fits-all process. Instead, it has become a strategic decision shaped by market conditions, corporate priorities, and the increasingly sophisticated demands of global investors.

Disclaimer

This article is published for informational, educational, and industry analysis purposes only and does not constitute investment, financial, legal, accounting, tax, securities, or professional advice. Capital market transactions involve significant risks, regulatory requirements, and financial considerations. Companies, investors, and stakeholders should consult qualified legal advisors, investment bankers, financial professionals, auditors, and regulatory experts before making decisions regarding IPOs, SPAC transactions, direct listings, mergers, acquisitions, or public market participation.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0