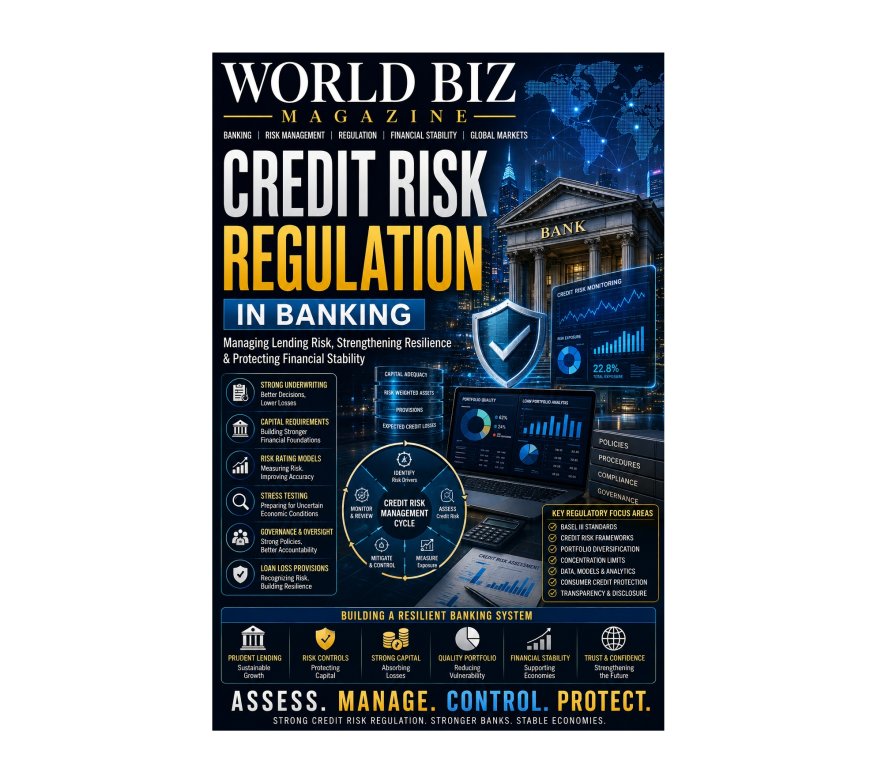

Credit Risk Regulation in Banking: Managing Lending Risk and Strengthening Financial Stability

Understand the role of credit risk regulation in preventing banking crises, improving resilience, and supporting sustainable lending practices.

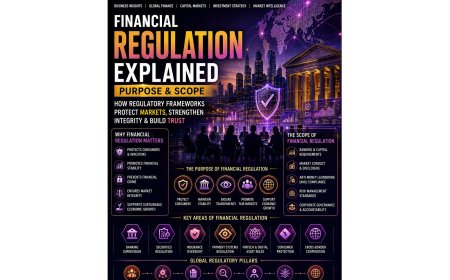

Credit Risk Regulation in Banking

How Global Regulatory Frameworks Manage Lending Risk, Protect Financial Stability, and Strengthen Banking Resilience

World Biz Magazine | Banking, Risk Management & Financial Regulation

Credit risk remains one of the most significant risks faced by banks and financial institutions worldwide. At its core, credit risk refers to the possibility that a borrower will fail to meet contractual obligations, resulting in financial losses for lenders. Since lending activities form the foundation of most banking business models, effective credit risk management has become a critical component of financial stability, regulatory oversight, and sustainable economic growth. From consumer mortgages and business loans to corporate financing and sovereign debt exposures, virtually every banking institution must manage the risks associated with extending credit.

The importance of credit risk regulation has grown substantially over the past several decades. Financial crises, banking failures, economic recessions, and periods of market volatility have repeatedly demonstrated the potentially devastating consequences of inadequate credit risk controls. Poor underwriting practices, excessive risk-taking, inadequate capital reserves, and weak governance structures have historically contributed to significant banking sector disruptions. As a result, regulators worldwide have developed increasingly sophisticated frameworks designed to strengthen lending standards, improve risk assessment processes, enhance capital adequacy, and reduce systemic vulnerabilities.

Today, credit risk regulation extends far beyond traditional loan approval processes. Modern frameworks incorporate advanced analytics, stress testing, capital requirements, portfolio monitoring, governance standards, provisioning requirements, and supervisory oversight mechanisms. Regulatory authorities expect banks to identify, measure, monitor, and control credit risk throughout the entire lending lifecycle. These requirements have become even more important as financial institutions navigate evolving economic conditions, digital lending platforms, artificial intelligence applications, and increasingly interconnected global markets.

Understanding credit risk regulation is essential for bankers, investors, regulators, policymakers, and business leaders seeking to comprehend how modern banking systems manage lending risks while supporting economic development and financial stability.

Understanding Credit Risk

Credit risk arises whenever a lender provides funds or extends financial obligations to a borrower.

The risk materializes if the borrower fails to repay principal, interest, or other contractual obligations.

Credit risk can affect:

- Commercial loans

- Corporate lending

- Consumer credit

- Mortgages

- Credit cards

- Trade finance

- Sovereign debt

- Project financing

Because lending generates a significant portion of bank revenues, credit risk management is central to banking operations.

Effective management protects both individual institutions and broader financial systems.

Why Credit Risk Regulation Matters

Bank failures often originate from poor lending decisions.

When borrowers default in large numbers, banks may experience substantial losses that erode profitability and capital reserves.

Unchecked credit risk can create:

- Institutional instability

- Liquidity pressures

- Reduced lending capacity

- Investor concerns

- Broader financial crises

Regulatory frameworks seek to reduce these risks by establishing minimum standards for risk management and capital adequacy.

Strong credit risk regulation supports confidence in banking systems and financial markets.

The Evolution of Credit Risk Regulation

Historically, credit risk assessment relied heavily on manual analysis and relationship banking.

Loan officers evaluated borrowers based on financial statements, collateral, industry conditions, and personal judgment.

Over time, financial markets became more complex.

The expansion of global banking, securitization, derivatives markets, and digital lending platforms increased regulatory concerns.

Major financial crises accelerated regulatory reform efforts.

The Global Financial Crisis of 2008 particularly highlighted weaknesses in credit risk assessment, underwriting standards, and risk governance.

Subsequent reforms significantly strengthened regulatory expectations worldwide.

Regulatory Objectives in Credit Risk Management

Credit risk regulations are designed to achieve several key objectives.

These include:

- Protecting depositors

- Maintaining financial stability

- Strengthening bank resilience

- Promoting prudent lending

- Enhancing transparency

- Reducing systemic risk

Regulators seek to ensure that banks maintain sufficient resources to absorb potential losses while continuing to support economic activity.

The goal is not to eliminate lending risk but to manage it responsibly.

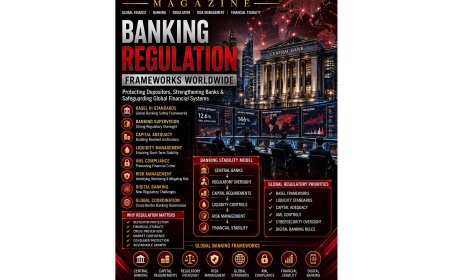

Basel Framework and Credit Risk Regulation

Global credit risk regulation is heavily influenced by standards developed by the Basel Committee on Banking Supervision.

The Basel framework establishes international principles governing capital adequacy and risk management.

Major regulatory milestones include:

Basel I

Introduced risk-weighted capital requirements.

Basel II

Enhanced credit risk measurement and introduced advanced risk assessment methodologies.

Basel III

Strengthened capital standards, stress testing requirements, and risk management expectations following the Global Financial Crisis.

These frameworks have become foundational elements of modern banking supervision.

Credit Risk Assessment and Underwriting Standards

Regulators expect banks to maintain robust underwriting practices.

Effective credit assessment involves evaluating:

- Borrower creditworthiness

- Repayment capacity

- Financial performance

- Industry risks

- Collateral quality

- Economic conditions

Lending decisions should be supported by objective analysis and documented processes.

Weak underwriting standards can lead to excessive risk accumulation.

Regulatory guidance emphasizes disciplined lending practices and consistent risk evaluation.

Risk Rating Systems

Modern banks typically utilize internal risk rating systems to classify borrowers according to credit quality.

These systems support:

- Pricing decisions

- Capital allocation

- Portfolio monitoring

- Regulatory reporting

Risk ratings help institutions identify higher-risk exposures and implement appropriate controls.

Regulators often review rating methodologies as part of supervisory examinations.

Effective rating systems improve risk transparency and decision-making.

Capital Requirements and Credit Risk

One of the primary tools used by regulators is capital regulation.

Banks must maintain capital reserves sufficient to absorb losses arising from credit exposures.

Capital requirements are generally linked to the risk profile of assets.

Higher-risk loans typically require higher capital allocations.

This framework encourages prudent lending and discourages excessive risk-taking.

Capital adequacy remains a central pillar of credit risk regulation worldwide.

Loan Loss Provisions and Expected Credit Losses

Banks must recognize potential losses before actual defaults occur.

Provisioning frameworks require institutions to establish reserves for anticipated credit losses.

Modern accounting standards increasingly emphasize expected credit loss models.

These approaches require forward-looking assessments based on:

- Economic forecasts

- Portfolio characteristics

- Borrower conditions

- Historical loss data

Provisioning enhances transparency and improves financial resilience.

Regulators closely monitor reserve adequacy.

Credit Concentration Risk

Excessive exposure to specific borrowers, industries, sectors, or geographic regions can create concentration risk.

Regulators encourage diversification to reduce vulnerability.

Examples of concentration risk include:

- Heavy exposure to real estate markets

- Industry-specific lending concentrations

- Large corporate borrower dependencies

Concentration limits help prevent localized problems from causing significant institutional losses.

Diversification remains a key risk management principle.

Stress Testing and Scenario Analysis

Stress testing has become a critical regulatory tool.

Banks are required to evaluate how portfolios would perform under adverse scenarios.

Examples include:

- Economic recessions

- Rising interest rates

- Property market declines

- Industry downturns

- Geopolitical disruptions

Stress testing helps identify vulnerabilities before losses occur.

Regulators increasingly incorporate stress testing into supervisory frameworks.

These exercises support capital planning and risk management.

Corporate Governance and Credit Risk Oversight

Effective governance is essential for managing credit risk.

Regulators expect boards of directors and senior management to maintain oversight of lending activities.

Governance responsibilities include:

- Risk appetite setting

- Policy approval

- Portfolio monitoring

- Internal controls

- Compliance oversight

Strong governance promotes accountability and supports sound decision-making.

Governance failures have often contributed to significant credit losses.

Technology and Credit Risk Management

Technology is transforming credit risk assessment.

Banks increasingly utilize:

- Artificial intelligence

- Machine learning

- Predictive analytics

- Alternative data sources

- Automated underwriting systems

These tools can improve efficiency and enhance risk identification.

However, regulators also monitor technology-related risks including:

- Model risk

- Data quality concerns

- Algorithmic bias

- Transparency issues

Technology governance is becoming an important component of regulatory oversight.

Consumer Credit Regulation

Consumer lending remains a major focus of credit risk regulation.

Authorities seek to ensure responsible lending practices and consumer protection.

Key regulatory concerns include:

- Affordability assessments

- Disclosure requirements

- Fair lending standards

- Debt management practices

Consumer protection frameworks help reduce excessive household indebtedness and support financial stability.

Responsible lending benefits both consumers and institutions.

Credit Risk and Economic Cycles

· Credit risk is closely linked to economic conditions.

· During periods of economic growth, default rates often decline.

· During recessions, credit losses may increase significantly.

· Regulators encourage banks to adopt countercyclical approaches that strengthen resilience during favorable conditions.

· This helps institutions withstand future downturns.

· Economic cycle management remains an important aspect of modern supervision.

Emerging Risks in Credit Regulation

Several emerging trends are influencing credit risk frameworks.

These include:

- Climate-related financial risks

- Digital lending platforms

- Artificial intelligence models

- Cross-border credit exposures

- Geopolitical uncertainty

- Alternative credit providers

Regulators continue adapting frameworks to address evolving risks.

Future credit risk management will likely become increasingly data-driven and predictive.

Global Regulatory Approaches

Although regulatory systems vary across jurisdictions, common themes exist worldwide.

Major banking markets generally emphasize:

- Risk-sensitive capital requirements

- Prudential supervision

- Stress testing

- Governance standards

- Portfolio monitoring

International coordination continues expanding through global regulatory organizations.

Cross-border consistency supports financial stability and market confidence.

The Future of Credit Risk Regulation

Future regulatory developments are expected to focus on:

- AI-enhanced risk supervision

- Climate stress testing

- Real-time portfolio monitoring

- Advanced analytics

- Digital lending oversight

- Enhanced capital planning

Technology will increasingly support both banks and regulators in managing credit risk.

The future regulatory landscape is expected to become more proactive and predictive.

World Biz Magazine Insights

Credit risk regulation sits at the heart of modern banking supervision because lending activities remain the primary source of both profitability and vulnerability within financial institutions. Effective regulatory frameworks help ensure that banks maintain strong underwriting standards, adequate capital reserves, diversified portfolios, and robust governance systems. As financial markets become increasingly digital and interconnected, credit risk management is evolving from a traditional banking function into a sophisticated discipline driven by data, technology, and predictive analytics. Institutions that successfully integrate regulatory compliance with advanced risk management capabilities will be best positioned to navigate future economic uncertainties while supporting sustainable growth.

Conclusion

Credit risk regulation plays a fundamental role in maintaining banking sector resilience and protecting financial stability. Through capital requirements, underwriting standards, stress testing, governance expectations, provisioning frameworks, and supervisory oversight, regulators help ensure that banks manage lending risks responsibly.

While credit risk can never be eliminated entirely, effective regulation provides the safeguards necessary to reduce vulnerabilities and strengthen confidence in financial institutions. As economic conditions, technology, and financial markets continue evolving, credit risk regulation will remain one of the most important pillars of global banking supervision.

Ultimately, strong credit risk frameworks not only protect individual institutions but also support broader economic stability by ensuring that lending continues in a prudent, sustainable, and resilient manner.

Disclaimer

This article is published for informational, educational, and industry analysis purposes only and does not constitute legal, regulatory, financial, investment, banking, compliance, tax, or professional advice. Credit risk regulations, capital requirements, supervisory expectations, and banking standards vary across jurisdictions and may change over time. Readers should consult qualified legal, regulatory, banking, and financial professionals regarding specific credit risk management and compliance obligations.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0